Key insights on reporting foreign inheritance to IRS effectively

Wiki Article

Understanding the Value of Reporting Foreign Inheritance to IRS for Tax Conformity

Steering the complexities of international inheritance calls for a clear understanding of IRS reporting responsibilities. Lots of people undervalue the significance of precisely reporting these properties, which can result in unintended repercussions. Falling short to adhere to IRS guidelines might result in large fines and legal issues. It is vital to realize the nuances surrounding international inheritances to stay clear of mistakes. The adhering to areas will make clear vital elements of conformity and the possible risks involved.

What Constitutes Foreign Inheritance?

When a specific obtains properties from a dead individual's estate situated beyond the USA, this transfer is considered a foreign inheritance. Foreign inheritances can include various kinds of assets such as genuine estate, savings account, investments, personal possessions, and company rate of interests. The worth and nature of these possessions may differ noticeably depending upon the legislations and custom-mades of the country in which the estate lies.Additionally, the process of acquiring these properties can include steering via international legal systems, which might enforce details requirements or tax obligations connected to inheritance. The recipient might likewise experience challenges in determining the reasonable market price of the inherited assets, particularly if they are not acquainted with the regional real estate or monetary markets. Understanding what constitutes a foreign inheritance is important for people to guarantee compliance with both neighborhood legislations and any potential commitments they may have in their home nation.

IRS Coverage Requirements for Foreign Inheritance

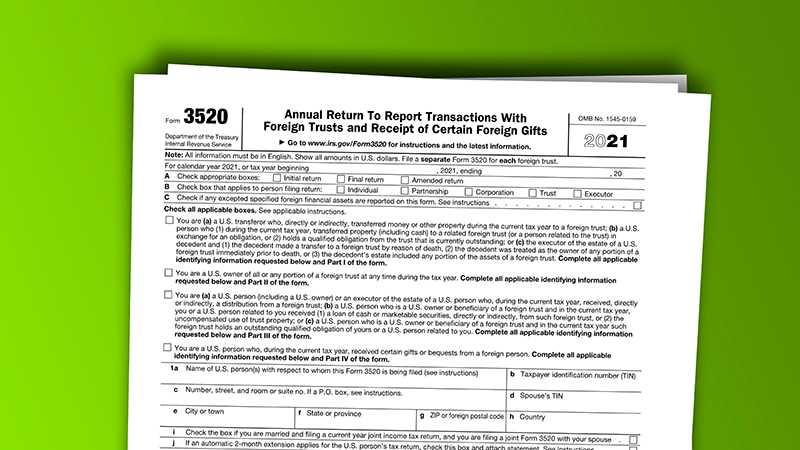

Exactly how does one steer through the IRS reporting needs for foreign inheritance? People who obtain an inheritance from abroad needs to recognize details reporting commitments to guarantee compliance with IRS laws. The Foreign Bank and Financial Accounts Record (FBAR) is one essential demand; if the total worth of foreign accounts surpasses $10,000 at any time throughout the year, it must be reported. Additionally, Type 3520 might be needed for reporting foreign presents or inheritances over $100,000 from non-U.S. persons. This type records details concerning the inheritance, including the resource and quantity. Failing to comply with these reporting demands can lead to substantial penalties. It is crucial for receivers to keep detailed records of the inheritance, including any kind of documentation from international entities. Consulting with a tax specialist well-informed concerning global tax legislations can give further assistance in guiding via these reporting commitments efficiently.Tax Effects of Obtaining an Inheritance From Abroad

Receiving an inheritance from abroad can carry significant tax obligation effects for people, particularly as they browse the complexities of worldwide tax legislations. The IRS needs united state people and homeowners to report foreign inheritances, which may trigger different tax obligations - IRS Form 3520 inheritance. Inheritances themselves are generally not considered taxable income, reporting is crucial to stay clear of fines.Furthermore, the estate might go through estate tax obligations in the foreign country, which could influence the web value received by the heir. If the inheritance consists of international possessions, such as realty or investments, they might feature special tax considerations, including possible resources gains taxes upon sale.

Individuals might need to comply with international tax policies, which can vary substantially from U.S. regulations. Comprehending these implications is essential for correct tax conformity and to assure that all commitments are met without sustaining lawful problems or unnecessary prices.

Usual Mistakes to Stay Clear Of When Reporting Inheritance

Steps to Guarantee Compliance With IRS Regulations

Understanding the steps necessary to ensure conformity with IRS guidelines is crucial for any individual reporting an international inheritance. Initially, individuals ought to verify whether the inheritance surpasses the reporting threshold, which can trigger added needs. Next off, it is essential to collect all pertinent paperwork, including the will, trust records, and documents of the foreign estate's value.Sending Type 3520, which particularly attends to foreign gifts and inheritances, is important to educate the IRS of the inheritance. People should also ensure that any type of appropriate tax obligations connected to the inheritance are paid, consisting of prospective inheritance tax in the international jurisdiction.

Additionally, maintaining accurate documents of all communications and transactions concerning the inheritance can give needed support in instance of an IRS questions. Seeking specialist guidance from a tax obligation consultant acquainted with global tax regulations can even more boost compliance and minimize risks linked with reporting foreign inheritances.

Regularly Asked Questions

What Happens if I Fail to Record My Foreign Inheritance?

Failing to report an international inheritance can cause significant fines, rate of interest on unpaid tax obligations, and possible legal consequences. The IRS may pursue enforcement activities, complicating future economic negotiations and compliance commitments for the private entailed.Can I Subtract Costs Associated With Receiving Foreign Inheritance?

No, expenditures associated with receiving reporting foreign inheritance to IRS a foreign inheritance are generally not insurance deductible for tax functions. Inheritance itself is normally not thought about taxed earnings, and linked costs can not be asserted to reduce tax obligation liability.Are There Fines for Late Reporting of Foreign Inheritance?

Yes, there are charges for late reporting of international inheritance to the IRS - IRS Form 3520 inheritance. These can consist of penalties and interest on unsettled tax obligations, making prompt disclosure important for conformity and staying clear of additional financial worriesHow Does Foreign Inheritance Impact My State Tax Obligations?

International inheritance might impact state taxes in different ways depending on jurisdiction. Some states enforce inheritance or estate tax obligations, while others do not. It is essential to seek advice from neighborhood regulations to identify particular tax obligation effects connected to international inheritance.

Are Presents From Abroad Thought About Foreign Inheritance for IRS Purposes?

Gifts from abroad are not identified as foreign inheritance for IRS objectives. foreign gift tax reporting requirements. Rather, they are treated individually under present tax obligation regulations, with different reporting requirements and thresholds that people should adhere to for complianceFurthermore, the procedure of getting these properties can include navigating via foreign lawful systems, which may enforce certain needs or tax obligations connected to inheritance. The IRS needs United state citizens and locals to report international inheritances, which might trigger various tax responsibilities. Submitting Type 3520, which particularly attends to international presents and inheritances, is crucial to inform the IRS of the inheritance. Failing to report an international inheritance can lead to substantial penalties, interest on overdue tax obligations, and possible lawful repercussions. No, costs associated to obtaining a foreign inheritance are generally not insurance deductible for tax obligation functions.

Report this wiki page